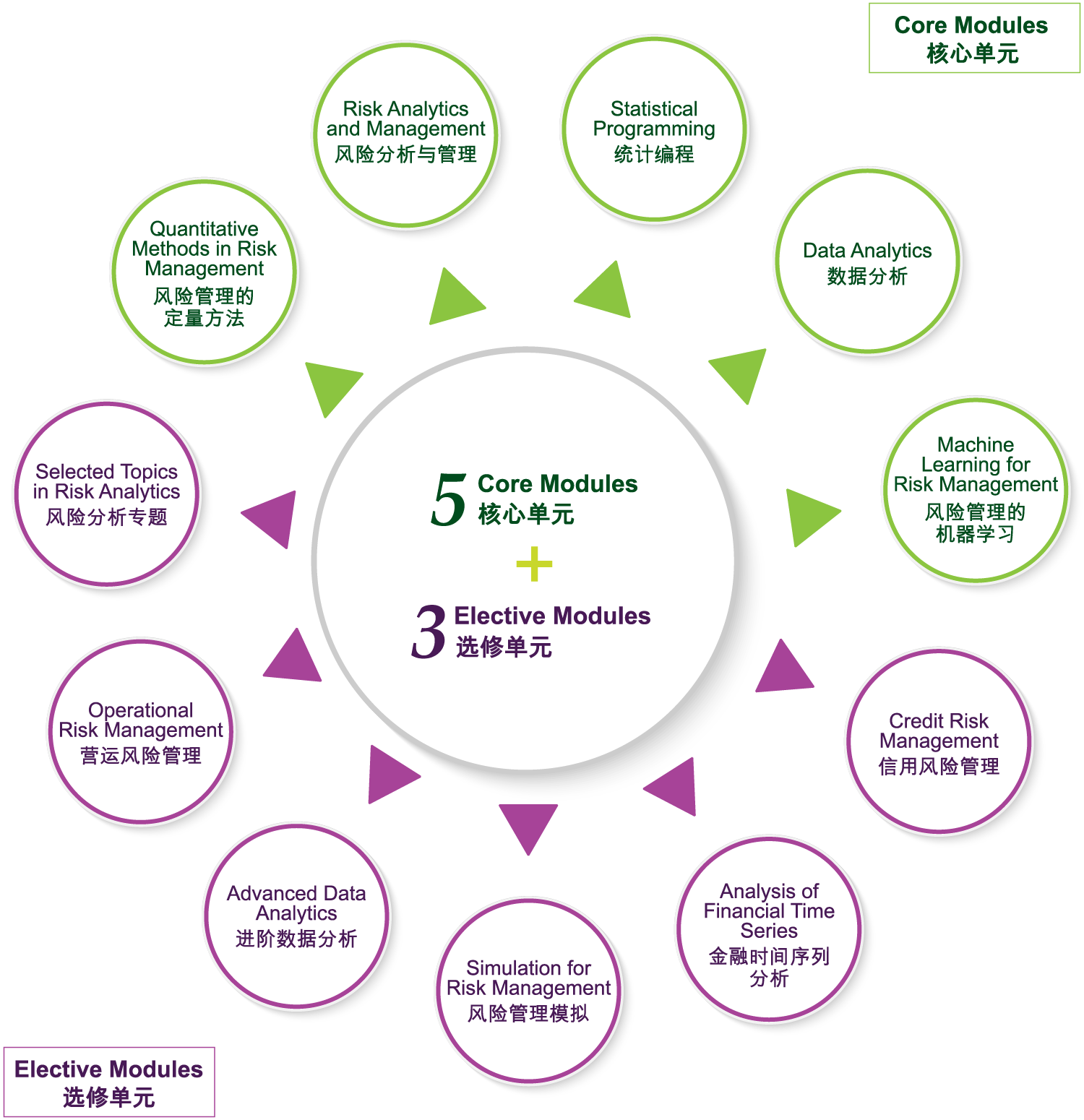

Programme Curriculum

The MSc-RA programme consists of two major parts: (1) five core modules; (2) three major elective modules.

Core Modules

This module introduces the use of applied statistical methodologies as a comprehensive approach in risk management. It provides students with the foundation knowledge to further apprehend in-depth material presented in other modules of the programme. Major topics include organisation and presentation of data in an informative way, some useful probability distributions used in statistical inference, estimation of parameters, hypothesis testing and basic regression analysis.

This module provides students with fundamental concepts of risk analytics and management. It introduces commonly used risk models in the financial industry and other business sectors. Major topics include market risk measures, risk measurement tools, risk analytic models and option Greeks for risk management. Students will learn how to practically implement risk analytic models with computer software to evaluate risks in the industries. Ethical issues related to risk management will also be discussed.

This module teaches programming fundamentals for risk analysts. Students will learn programming techniques with emphasis on data source connection, data pre-processing pipeline, exploratory data analysis, data visualizations and data reporting. Topics include basic concepts for programming, lists, objects and functions, matrix and data frame, use of programming packages and libraries, database manipulation, descriptive statistics, simulation and Monte Carlo methods, and statistical graphics.

This module aims to provide students with the data analytics techniques for solving practical problems in risk management. Students will learn a set of statistical tools for data visualization and apply data analytics techniques such as classification, association rules, cluster analysis and dimensionality reduction to analyse practical problems. Ethical issues related to the use of data will also be discussed. Students are required to work effectively in a team to complete a project.

This module provides students with the machine learning methodologies and algorithms for solving practical risk management problems. Major topics include supervised learning, unsupervised learning, hyper-parameter tuning, model evaluation, artificial neural networks, recurrent neural networks, reinforcement learning, and applications of machine learning to risk management.

Elective Modules (Choose 3 modules from the following)

The module introduces the principles of credit risk management. Topics include credit & counterparty risks, structured products, regulations, and other contemporary topics. Students will learn how to apply the quantitative methods to measure credit risks from the perspectives of investment managers, banks, regulators, and other financial intermediaries.

This module deals with the methodology and applications of business and financial time series. Topics include statistical tools useful in analyzing time series, models for stationary and non-stationary time series, seasonality, forecasting techniques, heteroskedasticity, ARCH and GARCH models, and multivariate time series.

This comprehensive module offers a deep dive into the field of simulation and its utilization in the realm of risk management. The course begins with an overview of the definition and historical background of simulation and highlights its significance in managing risk effectively. Through this course, learners will gain an understanding of the generation of random variables, including pseudorandom numbers, discrete and continuous random variables, and random vectors. The statistical analysis of simulated data will be explored in detail, including important concepts such as sample mean and variance, the construction of confidence intervals, and the application of bootstrapping techniques. To further enhance the accuracy of simulated data, the course delves into variance reduction techniques such as control variates, antithetic variates, variance reduction by conditioning, and stratified sampling. Lastly, the course concludes by examining other applications of simulation in risk management, including the evaluation of exotic options and the development of insurance risk models.

This module introduces various advanced methods for linear and non-linear models in data analytics, and discusses the mathematical principles behind them as well as their trendy real-life applications. Major topics include Principal Component Analysis, polynomial regression, spectral regression, kernel regression, logistic regression, Bayesian classifiers, Classification and Regression Trees, EM algorithm, MM algorithm. The implementation of the tools in statistical so ware will also be demonstrated.

This module aims to let students learn the state-of-the-art knowledge in the area of operational risk management. Catastrophic losses are usually caused by a combination of risks along with failure of risk controls, which is a form of operational risk. This course introduces some tools in operational risk management.

This module aims to let students learn the state-of-the-art knowledge in the area of risk analytics. It covers selected contemporary topics in related fields. The topics vary depending on the latest trends and the expertise of the module coordinator. It also emphasizes on practical knowledge, such as real-life examples and hands-on skills.

Study Plan for Full-Time Students

Semester 1

- AMS6101 Quantitative Methods in Risk Management

- AMS6102 Risk Analytics and Management

- AMS6103 Statistical Programming

- AMS6104 Data Analytics

Semester 2

- AMS6105 Machine Learning for Risk Management

- Three major elective modules

Study Plan for Two-Year Part-Time Students

Semester 1

- AMS6101 Quantitative Methods in Risk Management

- AMS6102 Risk Analytics and Management

Semester 2

- Two major elective modules chosen from AMS6106, AMS6107, AMS6110

Semester 3

- AMS6103 Statistical Programming

- AMS6104 Data Analytics

Semester 4

- AMS6105 Machine Learning for Risk Management

- One major elective module

Graduation Requirements

To be eligible for the award of the Master of Science in Risk Analytics, students are required to:

- complete and obtain a Grade D or above on at least 8 modules (24 credits), including five core modules and three elective modules; and

- obtain a minimum cumulative GPA of 2.0.